I was looking at some different data today (attached to this post), and it's showing some interesting numbers that might suggest we're near or already hit the bottom. The big question is... why?

Lending is tight, the economy isn't so great... so why are we here, if we are? Has it hit that magic price floor, or are people buying?

If the market is turning, why isn't the media all over it (somewhat of a loaded question if you've read my posts about the media usually being a couple months behind the curve when it comes to any financial market)?

These are things I am trying to establish, but one thing is for certain, it looks like it is turning, although the data is too limited to say so with any degree of certainty. If you review the data though, comparing price and volume, the sweet spot looks like April - May is where it started turning.

What I can empirically observe is only a tiny fraction of the reality, even though I observe what I would consider a nice cross section of the populous as it relates to certain areas.

The biggest observation, I don't know anyone who is trying to buy a new home for themselves. The only people I know buying are investors. Now, even though there are plenty of private investors out there, they still couldn't account for the move. What this leads me to believe is the institutional RE investors (reits, large private funds, etc) are gobbling up some property.

I am going to try to do some research on this angle, look at some current prospectus', etc... but the interim, has anyone else looked at this or have a buzz amongst realtors or others that smart money is accumulating property?

If so, this is a single for myself, more than anything, that its time to load up, while still being smart about it of course and getting the right deals to protect you in the event of a worst case scenario (being really wrong).

{kind=link}

{kind=link}

the fla mrkt

her in fla.we had a problem before with teachers,firemen,nurses and others in the work force affording homes,so even tho sellers are still in denial of prices dropping,they`ve dropped enuff that these ppl can now afford homes using 1st time homebuyers programs,and the investers are loading up too.lending is still tight, but FHA and others like FANNIE MAE and FREDDIE MAC are still available..also the developers are doing their part to unload.some that bought apartment complexes to convert to condos, are now backing away and remaining rental complexes.but we still have a huge backlog so deals are still out there,now if only I had a mentor to birddog for.LOL ,,Jim

Phoenix market

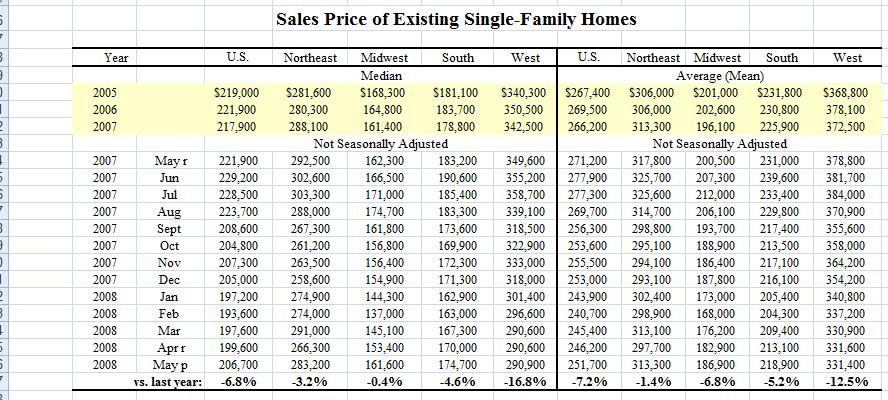

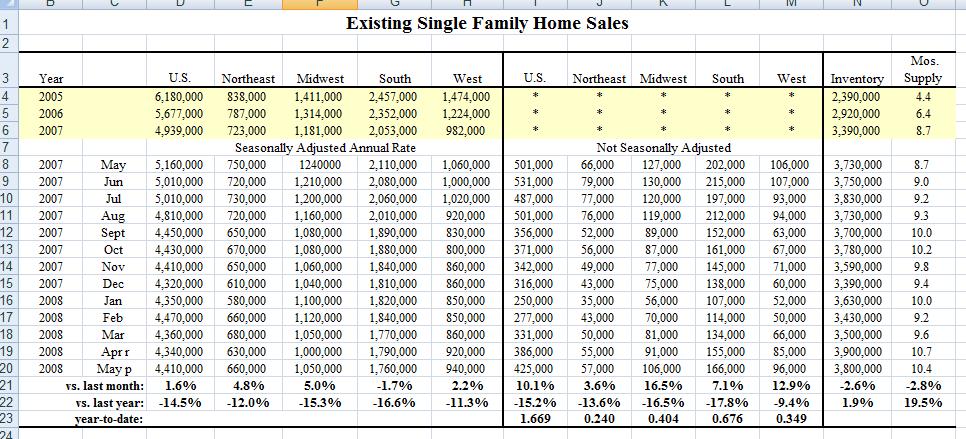

Maybe someone can help me interpret these numbers. The number of new listings has been pretty stable for about a year. The average listing price was stable from June thru Dec of 2007, but has decreased 13% in the last five months. The number of sales has increased considerably in the last five months, probably due to the price decreases. Sales are up 94%. May and June are top sales months in Phoenix. In 2007 sales raised 32% in same time period. The average sales price has been decreasing for ten months and is down 16% in the last five months. The number of REO listings is up considerably in the last six months, which caused the average listing price to go down. I believe the number of forclosures in this area will continue to rise for probably another year. I don't think our market has bottomed yet. What do you think?

Al

Phoenix

I was looking at the Phoenix foreclosure/preforeclosure numbers alone, and I interpreted those as the foreclosures hitting bottom.

In Phoenix, people are not trying to get out, they are trying to get in. When the foreclosure supply dries up, I think it's booming from current prices, but nowhere near previous highs. I think foreclosures there are starting to make the turn. Sure, there is plenty of them, but they are decreasing based on the two months of data I saw.

How the correlates to the rest of the market and data is up to anyone to decide, but you probably know what I am rooting for!

numbers?

Where did you get the forclosure/preforclosure numbers that you spoke of? I could not find that on the net. Also Phoenix was a little dofferent, in that our peak came later than most other areas. It has only been a couple years, so I am thinking that the forclosure issue will continue for another year. I this incorrect?

Al

Data

http://www.realtor.org/research/research/ehsdata

The peak and length does not correlate to any other market really. It is based on the factors in the local market that dictate the length and extent of events, like foreclosures.

You need to watch the trend of foreclosures/preforeclosures for Phoenix. The numbers indicate the bloodletting in Phoenix foreclosures have hit their peak. You want to get on the wave at that peak, and ride it down while home prices start to rebound.

I don't think a bulk of the REOs will be soaked up in Phoenix for another year, but that's thing, do you wait until the low lying fruit has all been picked to get it?

Thanks

Thanks, that makes sense, and thanks for the web link, I'll check it out.

fla. mrkt.

as I said sells are up in southeastern fla.There are institutional,pvt investors,and individual buyers making moves.also foreclosures are still going thru the roof.and the info is mixed,you have investors trying to unload and buy,you have homeowners pulling homes off the listings to wait out the bottom in pricing,and still over it all the lending is still tight.we have a very diverse work force so no 1 company moving or downsizing won`t hurt much.I`m looking at multi-units and SFHs.Seeing some good stuff but hav`nt been able to work anything out yet.Just visiting to get the hang of talking to sellers.

thanks Dean for the Site,God Bless you ppl.

Jim aka grandpa

Re: Real Estate Market Turning?

Dear DGAdmin,

I am so very new to the DeanGraziozi.com site and the world of investing, but since I purchased the TALD course and began looking at properties around my area (so. calif) here is what I have noticed:

1. The media has no clue about the market turning. If they had, then more new stories addressing the subject would be appearing.

2. Lending at sub-prime rates: if they continued to be made during or up to the year 2007, that may explain why I am STILL seeing home prices, condominiums, dropping in my local area ( down as much as $15,000 in the last 3 months ). If no one can afford their homes, they default. Then the value of homes around theirs are affected as well. Then news reports make note of low consumer confidence in the housing market, and word spreads. My guess is that mortgages with low subprime rates are still coming due, people will continue to default on their loans and will continue to do so, the rest of this year.

3. Election time: Notice the low rates on Certificates of Deposits vs. Treasury Bills.

I was talking with a local bank representative who I do business with on a regular basis, and it was explained to me the Fed Reserve will keep rates low until after Election Time - it was explained to me this occurrence happens regularly in an election calendar year. Well, CD rates have been LOW since this Spring.

4. The Bottom. I believe we are moving into the Bottom but that we are still experiencing the effect of property values "Settling," if that's an appropriate way to describe the progression.

I believe it's a 'holding pattern' new buyers are in now, and they are holding their money. Why buy a new home if the Value in it is not equal to but "less" than the actual Equity that would be earned in a purchase? [ Yes, WE ALL HERE know what to do, (hold, refinance at a low interest rate, rent in the meanwhile, and be ready to sell when the home market turns into an upswing). But how to impart all that we learn HERE into the Real World? My answer: ONE GREAT DEAL AT A TIME. When we make a purchase we bring a creative deal to the table. And everyone wins. ]

5 Conclusion: We are in a "settling" and "holding pattern." I think this is true because the Government has not found a true solution of how to loan money to new buyers AND make the lending practice "FAIR" to everyone.

DGAdmin: I believe you are right about REI's buying up available properties which laypersons may not be aware, and even if they were, the current market (economy) has not provided them with the knowledge or information necessary for them to do so. Case in point: Me. I did not know ANY of the things I have learned and am learning since joining the TALD program and this site ( just two weeks ago ).

Very Sincerely,

-quicksilver

Now that's what I call - Success!

Sources:

1)

http://promo.realestate.****/home-for-sale-by-any-means.html

2)

http://realestate.****/Foreclosures/44ffca03769cc83668366e203a1a7da2

3)

http://promo.realestate.****/weakest_us_housing_markets.html

Good points...

Good points! The issue with the lending is not so much a government issue they have direct control over. I mean, they are revising lending practices so the predatory lenders have to jump through more hoops to prey, but the tightness is on the banks and the secondary markets the mortgages are traded in.

No one wants real estate backed paper in the financial markets unless it is AAA. Anything else, particularly when it is used in derivitive based investments, it is hard to mark to market, and is also seen as pretty risky. That is why lending has tightened so much, real estate backed paper is in less demand and the ways they are able to extrapolate the investment potential of it has been diminished.

The government is trying thaw out the deep freeze in the financial markets by trying to pass a bill to guarantee bad paper and allow mortgage holders to relock in to better terms.

The underlying issue though is confidence... when stock holders don't have confidence in paper, they don't want to buy stock of companies that hold it. And so and so forth... when real estate re-emerges as solid asset again, lending loosen back up. Not like it was, but loosen to a realistic level.

The gov't may be able to create confidence in the paper by backing it at the expense of the national treasury, tax payers and ultimately the US Dollar, but the rebuilding confidence in the real estate market is the real solution to the problem in my opinion.

near bottom on market in alaska

i heard the same thing on the low part on the market up here, i heard a stat from two diffrent realtors that our midrang homes from 150,000 to 250,000 has increased in value 2% this year although sales are still off 40% to 50% for the realators . i just heard this this last week .

mike

Real Estate Market Turning?

Hi DGAdmin and All,

And just look - right when you post this very interesting Question DGAdmin, look what comes up in the headlines: A mention of the overpriced homes. Built in 2006-2008, these "construction homes" have reduced in price because of 1) the slowed housing market, and 2) the glut of newly constructed homes which must be sold: good news for new home buyers! This means the New Construction Homes are actually "Cheaper" than the Value of Sellers' current homes. Yes, the Sellers will take a cut, to compete with the overstock, so to speak, but that incredible Mansion they want? Guess what, when they sell, it is 'affordable' because it is now worth 'less' than it used to be!

Entry-level new buyers can reenter the buying market, with help of possible FHA loans, etc., while Sellers who have dwindling property value, can sell their homes at a lower price, still make a profit, and take the same advantage of moving into a comparatively lower-priced, larger, New Home. (But WE HERE, through Dean's Book, TALD Course, and DeanGraziosi.com Resources, already knew this, didn't we? That's Awesome!)

Summary. I noted that either something in the housing market must change with a) the Fed Reserve, which you pointed out, only has so much they can do to 'curb' lending practices b) the big change would be - lower the prices of the homes and fix some low interest rates across the board - for everyone. And with great respect to everyone Investing and/or Buying: To put it succinctly, I think this thread has been saying what was being said all the time, albeit, unspoken - - Duh!"

Every Time I sign on to learn about Real Estate, I am Amazed at how "on-point" this site is and the materials we have at our disposal that can make everyone, including a novice, like me, so knowledgeable, so fast!

Thank you Dean and Everyone Here.

I LOVE YOU ALL!

Way Sincerely,

-quicksilver

Now that's what I call - Success!

P.S., Even without any news about the Housing Market, though it's nice to have, I absolutely love that we all know what to do and how to buy, regardless of any market situation, and through this site we help each other find creative ways to Succeed!

Additional References:

1) New Plans To Protect Home Buyers Associated Press http://news.****/s/ap/20080708/ap_on_bi_ge/fed_credit_crisis

2) On the Path to a Housing Rebound CNN Money

http://promo.realestate.****/on-the-path-to-a-housing-rebound.html

3) Home Refinancing Basics:

http://realestate.****/info/guides/home-refinancing-basics

MSNBC

FYI,

Just today the Associated Press says:

"Housing market slump seen stretching further."

Realtor group's top economist: 'We are not out of the woods by any means'

READ FULL STORY AT:

http://www.msnbc.msn.com/id/25591213

Experts said, Realestate will start rebounding in 2009.

Regards, Rohn Everson

DeJor Properties, LLC

House Market Turning?

Also, what is so interesting about the MSNBC report is "how" economists are suggesting the effects will turn: One economist, suggesting the slump may last through 2010, with the home market continuing to bottom out, while the National Association of Realtors’ trade group chief economist positing, as you already said: "...we are not out of the woods by any means.”

But my continual interest? The Lenders. Notice the regulator for Freddie Mac and Fannie Mae attempts to reassure investors,

'... an accounting rule change wouldn’t force the government-chartered mortgage finance companies to raise tens of billions in capital to offset losses.' [article, 'Housing Slump Stretching Even Further,' Associated Press, July 8, 2008. source; http://www.msnbc.msn.com/id/25591213 ]

Yet this week, Lender Indy Mae is slashing its workforce already: by stopping new loan submissions it is trying to build capital to stay afloat.

http://www.msnbc.msn.com/id/25582345/

So interesting. Since home loans are above 6% ( for now ), just How is the new home buyer base supposed to be any more convinced to buy new homes.

If persons could not qualify for the past Loans which still may be coming due as of present, and the Lenders become "regulated" to tighten even more on lending to everyone who deserves a chance to own a home in the first place, how will new home buyers buy? Talk about Low consumer confidence.

I say, since the home market prices are lowering, lower the loan rates. Fix loan rates for a definitive period of time, and keep them LOW. Of course The economy WILL recover, eventually, no matter "what" happens; maybe doing this would help it to recover more unilaterally.

I'm just happy I am part of this website and have Dean's course. What a better way to steer through any Economy!

[ I am going to buy a pair of rose-colored glasses now. ]

]

Yours Truly,

-

quicksilver

Now that's what I call, Success!

NW Iowa Market has not faultered, much

Lots to ponder here.....

Nevertheless, the market has not changed much here in the North West corner of Iowa! Still very few foreclosures, little to no sheriff sales, little interest in non-conventional mortgages and the housing market was never bloated to begin with BUT the good new is; we just lost-out on our third property since we started in April and WE WILL BE SUCCESSFUL in the end. On to the next property, a 4-Plex, wish us luck!!!!!

Ultimately, us REI's need to keep our course, stay positive, be dilligent, and run our businesses with integrity.

Regards,

Rohn & Shelley

DeJor Properties, LLC

where can i find some low priced homes

Is there any foreclosures that are selling for 30 cents on the dollar?

Turning Market?

From this post, it appears there are national factors such as what's happening with subprime financing and that would have a tendency to slow those first time buyers across the board. Also, the general trend of folks still moving to the Sun Belt means that metro areas north will tend to shrink and metro areas south will tend to swell.

Finally, state law differences and regional and local business growth will impact local REI (I'm thinking of Dejor's NW Iowa and my area in particular) and so there will be smaller areas in the middle that seem to be status quo...

Thoughts?

Yet ppl lack understanding

The bubble burst was merely a mass liquidation of property that does exist purchased with money that doesn't exist. When a bank loans you money for a house, they don't actually have to have the money they loan. Every bank is chartered with say, $1,000,000. Yet, they are capable of loaning out $10,000,000 when they only actually have $1,000,000. When you take out a mortage on a home from the bank, the money the bank gives you may not actually exist, and yet, they stick you paying interest on money that never existed until you took out the loan and they wrote the money into existence. Essentially, they can loan you air, and charge you interest on it. How interesting it was, a few years ago, these large lending institutions were pushing adjustable rate mortgages like every day on the tele. The crisis was set up, and it was only made worse by infinitely increasing inflation due to high energy prices which have also been a contrivance, and a doubling national debt. The crisis was loaded up, and as Ben Bernake went on record saying to the Mises Institute I believe it was, the Great Depression was caused by the private central back misleadingly called the Federal Reserve. The Federal Reserve is no more federal than federal express. Anyone ever thought about how strange it was that less than 30 years from the inception of the Federal Reserve, we had the Great Depression? The booms and busts are artificially created, and the American people lack understanding of this obvious reality. Anyway, that's my 2 cents. Another thing I find disgusting is the fact that over a 30 year mortage on one home, you are effectively buying 3 homes for the privelege of living in one. This is made even more disgusting by the fact that the mortgage on your home the bank loaned to you may not even exist. They loaned you money that doesn't exist which you have to pay back 3 times over with money that does or else they foreclose on your house and acquire real property from a default on a loan of money that didn't ever exist. It's shameful. The net result is, what? We have become as slaves to the system. We have to work more and more hours and more and more jobs for less and less money after inflation, energy, and cost of living increases consumes more and more of our paychecks, and get so deeply indebted we're forced deeper and deeper into indentured servitude. The system is sick when you look at it for what it is.

Rate of house price declines slows in 2nd quarter

I came across a great web site with an article about changing house prices. There are charts and stats on all states. Check it out at www.ofheo.gov/default.aspx.

Al

gov

what you say is so true.but the gov wonts to own everything and we work like dogs to feel like sombody. gov wins wee lose but the people are starting to wake up .but eny way you all have a great day.may god bless all

Spring Market and the time to buy is now

It is intersting to see how the market has changed during the past several months. So many people wonder if we are at the bottom of the market, however with first time home buyer incentives and Spring weather people are beginning to buy again in our Mid-west area. It will be intresting to see what develops during the next few months, however the time to buy is now. Buy as many properties as you can (as long as they cash flow themselves) before the market rebounds. Believe and Achieve!

How low will it go?????????

Looking back on comments from july 2008.

Things have definately gotten worse for homeowner's. Was listening to some news show where they were still saying things are not looking up. Now they are saying that there is a whole new era of foreclosures coming to head. Families who were living comfortable with good credit, with fixed rate mortgages. The show had a panel of advisors suggesting they bail out to save ther credit and move on. Instead of doing a modification on the mortgages if their income level is not going to support them in the near future. That means to me negotiation quickly! So this only confirms were in the right place and time.........Much success.

Lubertha

NJ real estate

As a Realtor here in NJ, I saw an artificial "bump" in the market at the end of the year ('09) which I attribute to the 1st, first time home-buyer's tax credit. However, this spring, I don't see as much activity here with only 33 days left to take advantage of the extended credit. Investors looking for second homes (vacation homes) are jumping this spring because they realize that this is probably their last chance to take advantage of the "perfect real estate storm" with prices AND interest rates as low as they are. There is a lot of speculation that mortgage interest rates are going to continue to creep up in the second, third and fourth quarters of this year. This is all still good news for us as REI's who are all trying to "think outside the box". The investors are buying, which is a good sign of things to come. However, I see a lot of banks (especially BOA) making things very difficult for home owners to get out from under their properties (short sell them) which I can see leading to another wave of foreclosures here in South Jersey. We are all faced with great opportunities to help sellers and make some money while doing so. God bless...